“The Wall” and Its Potential Impact on Cement Consumption

The following is a Portland Cement Association (PCA) Market Intelligence analysis of potential impacts to cement consumption associated with building a wall along the border of Mexico that is being considered by the Trump Administration. For context, the land border with Mexico crosses four U.S. states, spanning 1,933 miles: California (140 miles), Arizona (373 miles), New Mexico (180 miles) and Texas (1,241 miles).

Total cement consumption attributed to the construction of a wall would represent only a fraction of total U.S. cement consumption.

Prior to the boom period of 2004-2006 that was ignited by low and exotic mortgage rates, the cement industry averaged slightly more than 100 million metric tons (Mt) of cement consumption annually. Using this level as the basis, construction of the wall as defined by PCA would amount to less than 1 percent of total national construction. The wall’s construction, however, is a regional phenomenon focusing on the four border states.

Natural barriers may reduce the coverage of the wall.

Natural barriers may reduce the coverage of the wall, given the border between the U.S. and Mexico includes rivers and mountains, which account for 973 miles of border. This reduces the “wallable” border 960 miles. Natural borders include Arizona (19 miles) and Texas (954 miles). California and New Mexico have no natural borders.

Man-made barriers already exist along the border, potentially reducing the length of a wall.

Man-made physical barriers of entry into the U.S. from Mexico already exist along some portions of the border. By state, these barriers include California (140 miles), Arizona (324 miles), New Mexico (120 miles) and Texas (160 miles). Some of these barriers include fences and vehicle barriers. Some of these barriers may, or may not, constitute wall criteria according to the Trump Administration. PCA assumes these barriers are a sufficient barrier and meet the Trump Administration’s definition of the wall and will not need additional investment.

Texas represents the major area of wall construction.

Considering the border mileage, and subtracting out natural and existing man-made barriers suggests that wall construction represents 217 miles – far different than the nearly 2,000-mile border believed by some. Of this, 127 is attributed to Texas, New Mexico (60 miles), Arizona (30 miles) and no construction required in California. These estimates all depend upon the definition of a wall. PCA’s assessment may be a liberal interpretation due to its inclusion of fences and vehicle barriers.

The size of the wall has significant impact on associated cement consumption.

There is no indication as to the wall’s material specification. Steel, concrete or a combination of both, are the likely materials used. Since this analysis is to determine the ability of the cement/concrete industry to meet potential assessments, we assume all construction will be concrete.

Dimensions of the wall contribute to potential cement consumption attributed to its construction. PCA considers a high and low scenario regarding the dimensions of the wall. The lowest height of the wall is assumed to be 20 ft. The highest height of the wall is assumed to be 60 ft. The lowest width of the wall is assumed to be 8-in. thick. The highest width of the wall is assumed to be 12-in. thick. PCA takes these dimensions and combines them with the typical amount of cement/concrete used for this type of construction by area and then combines them with the miles to be construction to form the basis of cement consumption required for the walls construction.

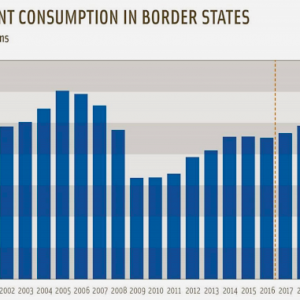

Consumption among border states remains depressed compared to past peaks.

Cement consumption among the four border states declined 13.9 Mt, or more than 46 percent during the recession – peak-to-trough. Since then tepid recovery in the economy has added 6.3 Mt to cement consumption. This level, however, remains 25 percent below past cyclical peak levels.

Capacity utilization rates in the border region are low.

As a result of the slow economic recovery among border states, utilization rates remain low and may offer significant opportunity to supply wall material requirements. The bordering states’ clinker capacity totals 25.7 Mt and is currently operating at 77.1 percent utilization. This implies nearly 6 Mt of unused capacity annually. Even if real world operating rates reduce utilization to 90 percent, nearly 3.5 Mt of domestic capacity exist to supply near-term demand.

Capacity in southern California is estimated at 9.4 Mt annually. Based on 2016 levels of production, these plants are running at 79.6 percent utilization. Arizona and New Mexico’s combined capacity is 3.3 Mt and currently operating at an estimated 61.4 percent utilization. Finally, Texas has a production capacity of more than 13 Mt and is running at 79.3 percent utilization.

Most cement engineers suggest that cement kilns can run as high as 90 percent utilization rates for a sustained period of time. Given this, slack capacity still exists given the magnitude of the volume impact associated with the recession and tepid economic growth since the recovery.

Total incremental cement consumption related to a wall may not be as large as many suspect.

If all barriers already in place along the border (fencing and vehicle barriers) are subtracted, then the mileage of wall construction implied by the Trump proposal shrinks from roughly 2,000 miles to less than 220 miles. The definition of what constitutes a wall, therefore, has large implications regarding the incremental additional amount of cement consumed due to the wall’s construction. Once these assessments are determined, additional assumptions must be made regarding the material specification, height and width of the wall. PCA’s assumptions and cement consumption estimates by border state are summarized below. It is likely that these total consumption volumes will be spread over several years of construction – further minimizing the possibility of supply strain.